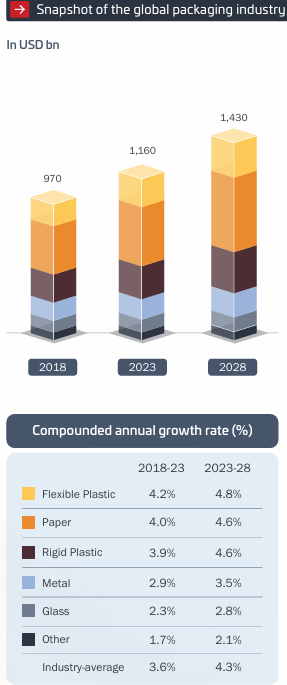

India’s domestic packaging industry is expected to grow at about 9% CAGR over the next five years, reaching US$ 92 billion by FY30, states Investment bank Avendus Capital in its latest report, which highlights the sector as a key beneficiary of the country’s consumption-led growth, with rising investor interest and deal activity across segments.

According to the report, seen by PSA, India is now the world’s fastest-growing packaging market, projected to outpace GDP growth by 1.3x, driven by rising demand from end-use segments such as food and beverages, pharmaceuticals, personal care, agriculture, durables and e-commerce, along with growing penetration of organized retail and quick commerce.

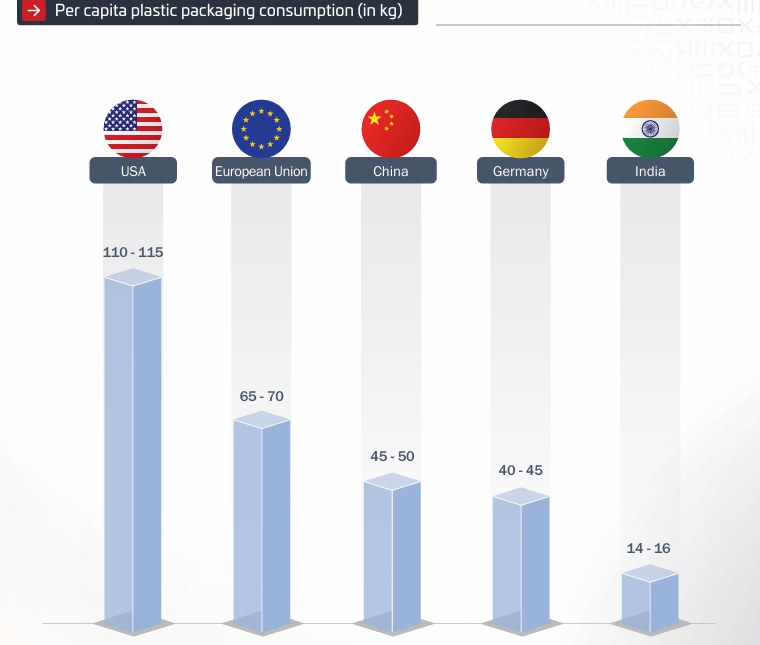

Globally, packaging is already a US$ 1 trillion industry, making it one of the largest manufacturing ecosystems across paper and board, plastics, metals, glass, and composites. In India, per-capita plastic packaging consumption remains materially underpenetrated compared to developed markets, with the US at nearly 7x and Europe at around 4x, signaling strong headroom for growth.

Among substrates, rigid plastic packaging (RPP) stands out as the fastest-growing segment in India, set to grow at 10.3% CAGR over the next five years, owing to its durability, cost efficiency, and suitability for mass distribution.

Flexible plastic packaging (FPP) remains the largest segment, accounting for 27% of the Indian packaging market, supported by strong demand from packaged food, FMCG, personal care, and pharma.

Beyond plastics, the report sees paper gaining from the shift toward recyclable, fiber-based materials, while glass and metal packaging are expected to witness growth at 7.5% and 7% CAGR, respectively.

Koushik Bhattacharyya, managing director and head, Industrials Investment Banking, Avendus Capital said, “The packaging industry has emerged as one of the strongest proxies to India’s consumption growth. Moving well beyond its traditional role as functional input, packaging is now being leveraged to enable high-value differentiation through branding and customer experience.”

“With rising incomes, premiumization, and formalization of retail and supply chains, the Indian packaging industry is structurally well-positioned to serve a broader shift towards organized and branded consumption. We believe these structural tailwinds will continue to drive deal activity, consolidation, and capability-led scale building, keeping the sector firmly on the radar of both strategic and financial investors.”

The report highlights sustainability as a major structural theme. While flexible packaging remains critical due to its low per-unit material usage, recycling rates in India are still below 10%, highlighting a significant gap.

Regulatory tailwinds, including Extended Producer Responsibility (EPR) norms, are accelerating the adoption of recyclable and eco-friendly materials. In response, Indian consumer companies are increasingly shifting from multilayer laminates to mono-material and recyclable structures, it states.

In India, deal activity has remained steady over the past decade, with increasing participation from private equity and strategic investors. Financial sponsors have accounted for 76% of minority transactions and 25% of majority transactions, reflecting growing investor confidence in the sector’s long-term growth potential. As the industry evolves, M&A is expected to play a key role in driving scale, enhancing capabilities, and enabling entry into high-growth segments and geographies.